November 2021

In the 2000 comedy, Meet the Parents, Ben Stiller’s hero tries desperately to impress his girlfriend’s parents. He undermines his efforts with various blunders that are only compounded the harder he tries to fix them. For example, when he lets the indoor cat onto the roof and tries to recover him, he ends up not only losing the cat but lighting the backyard on fire as well.

To a large degree, the current economic environment also feels like a product of unintended consequences as central banks keep trying to smooth over economic hiccups with more stimulus, only to exacerbate the problem. The Federal Reserve (“Fed”) started its massive money printing campaign after the 2008 financial crisis. Last year, 2020 marked a shift, where it wasn’t just the central bank but Congress also that jumped in and provided unprecedented stimulus to combat the pandemic that shut down the economy. Any arguments on whether this level of stimulus is necessary are academic given that we are in a world where there is no will for fiscal austerity or even moderation. Instead, the more relevant issue is examining the unintended consequences of this stimulus and what it means for investors going forward.

Asset Prices Are Expensive

The third quarter was a bit of a mixed bag for equity markets, with large U.S. companies in the S&P 500 edging out a modest 0.6% gain after losing around 5% in September. Smaller U.S. companies and international stocks had negative quarters. The year-to-date stock returns are still obviously robust, while core U.S. bonds are floating in modestly negative territory. The broad commodities index had another strong quarter and is now up nearly 30% for the first nine months of the year.

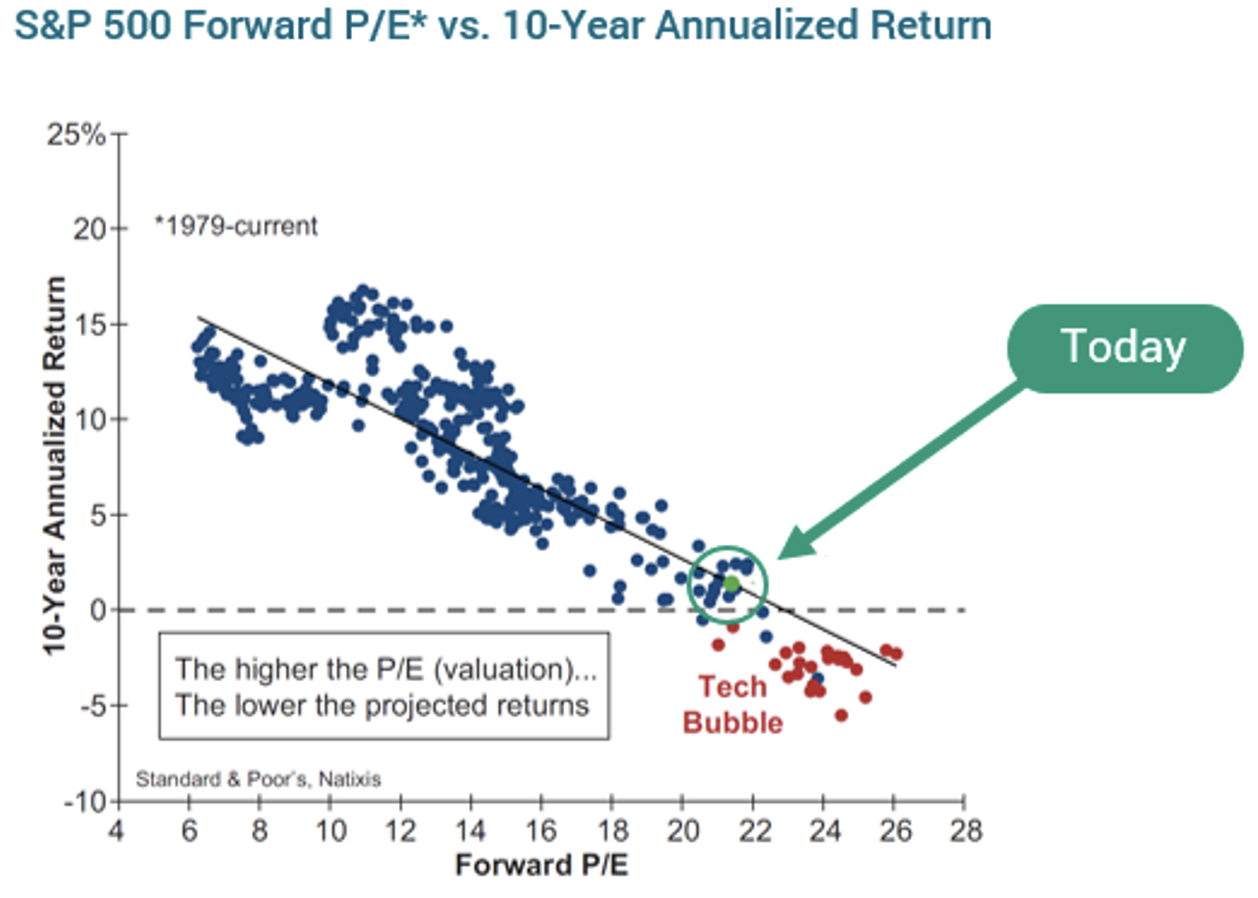

The mixed quarter did little to detract from expensive valuations across the globe. Arguably, it is easy money from the Fed, as well as from across the globe, that has led to expensive valuations in financial assets like stocks and bonds. When viewed with a historical lens, valuations have been meaningful indicators of future expected returns. The below chart illustrates how higher P/E ratios (valuation measures indicating how cheap or expensive markets are) at a given point in time have historically resulted in lower future returns.

The historical data is very clear: Markets that started with cheaper valuations, or those data points toward the left side of the chart, saw higher returns over the subsequent 10 years. The green dot on the lower right side of the chart shows us where we are today, with valuations that are very expensive relative to history. If the next 10 years were to be in line with historical precedent, stock investors could expect returns of around 2% per year.

This chart is not saying that high valuations are effective timing tools, because they are not. Stock prices can remain expensive for extended periods of time. However, they do reflect an investor’s level of risk. Current valuations do not necessarily mean that this is a market top, but based on history, today’s investors have very little margin of safety.

What about bonds? Government policies keeping interest rates low and printing money have also made this asset class expensive and unattractive for quite some time. In fact, across most of the globe, government and other “safe” bonds are literally yielding nothing. Now, even lower quality companies, where both the risk and yield have historically been higher, have seen yields driven down to bottom-basement levels. With the recent jump in inflation to over 5% annualized, more than 80% of these so-called “high-yield” bonds are yielding less than inflation. Even if inflation levels off to a more tolerable 3% level, 35% of today’s high yield market would still not meet that threshold.

Why would an investor want to buy a risky bond where, even if things worked out perfectly (i.e., there was no default), they wouldn’t make as much as inflation? This is indicative of how government policies are forcing desperate investors to do whatever they can to find yield, driving up prices and valuations to unattractive heights. Investors are willing to tolerate the current situation because they believe that inflation will adjust downward, but what if inflation stays elevated for an extended period of time?

Governments Are Trying to Clean Up the Mess They Made

Despite assurances from the Fed that current inflationary pressures are transitory, there are more and more signs that elevated inflation will be around for longer than originally expected. Supply chain disruptions, labor market shortages and massive increases in housing costs are all foretelling higher levels of inflation for at least several quarters to come.

In response, the Fed recently announced that it will begin “tapering” its asset purchases in November. These asset purchases have been major contributors to inflationary pressures, so this would seem like a step in the right direction. While that may be the case, when the Fed talks about tapering, it isn’t talking about interest rate hikes or selling assets to try and put the brakes on inflation. Instead, it means that it will gradually reduce some of the excess stimulus it has been pouring into the system.

But the damage may very well have already been done. Prior to the 2008 financial crisis, the Fed’s balance sheet was less than $1 trillion; today, it has increased by roughly 10 times and now exceeds $8 trillion. All this money was created out of thin air and was used to purchase assets to stimulate the economy and keep interest rates, or borrowing costs, low. Buying a little bit less at this point doesn’t change the fact that the system is already flooded with liquidity. And realistically, it’s not feasible for them to stop printing money entirely when you look at the trillions in annual budget deficits we now regularly run in our country. If this government spending is to proceed, the Fed will need to make up the deficit with the magic of the printing press.

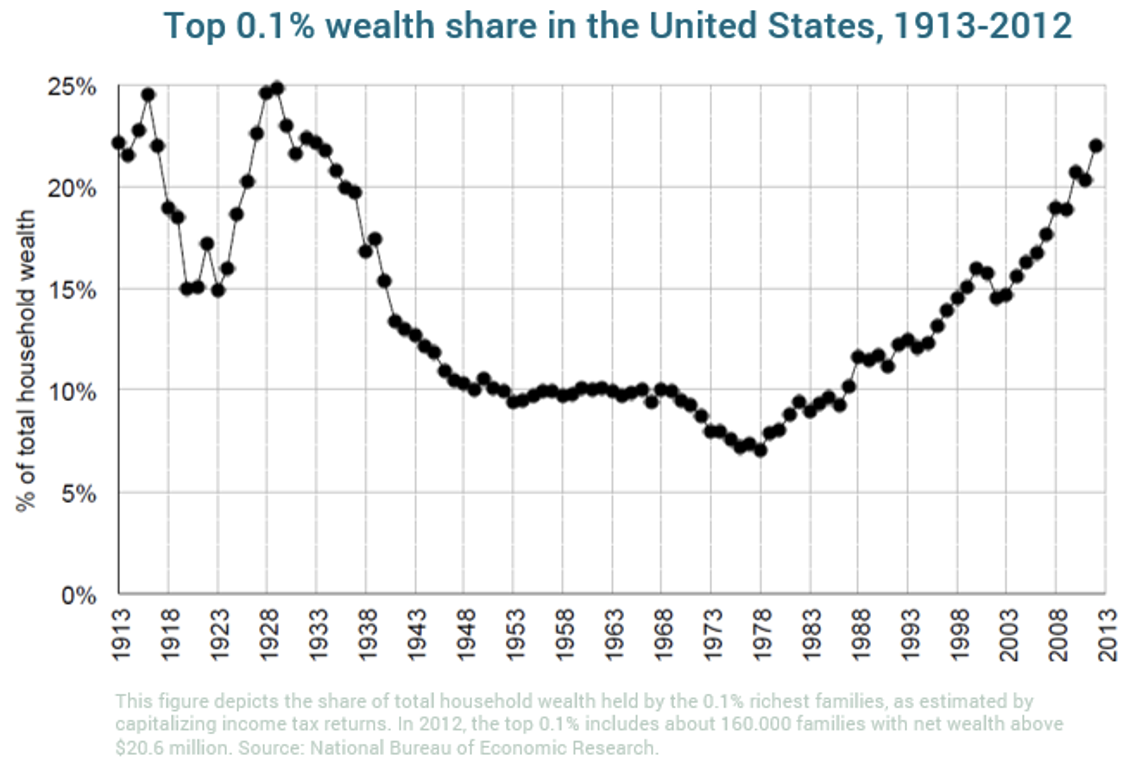

Beyond inflation, government policies have also exacerbated the wealth gap. Their policies pushed up prices in assets such as stocks, bonds and real estate, essentially making it so that anyone who started with assets got richer and anyone who didn’t have assets was left behind. The below chart goes back to the early 20th century, showing the percentage of wealth in the U.S. that is controlled by the top 0.1% of the population.

The wealth gap has been at these extremes before, back in the early 1900s. Now, government policies have driven us back to the highs. While this chart focuses on the U.S., this is a global problem as well. Today, 1.1% of the global population controls almost half of global wealth. The bottom 55% of the population controls only 1.3% of global wealth.

The government inflated asset prices and exacerbated the wealth gap, and now it is trying to come up with policy responses to narrow that gap. The recent proposals surrounding changes in estate and income tax law, combined with the aggressive spending plan they accompany, are the most recent such responses. Whether our dysfunctional government can actually pass any of these measures is still in question. Regardless of what any final legislation looks like, though, it must be noted that there is tremendous societal pressure for the government to narrow the wealth gap it helped create.

How Can Investors Protect Themselves?

Government policies and inflation are two risks over which investors don’t have any direct control. However, investors can control how they prepare for these eventualities. Changes in government policies may be unpredictable but creating a comprehensive financial plan can help with both flexibility and peace of mind. Spending the time up front on planning can help identify weak areas in someone’s financial picture and help empower that individual to address any identified risks.

On the inflation front, it’s important to diversify into asset classes that have historically been more resilient in inflationary environments since traditional stocks and bonds are not necessarily the best solutions. While certain stocks may be able to keep pace with inflation if they can pass increasing costs on to consumers, this is more easily said than done. Traditional bonds with low fixed-rate coupons will be the hardest hit in an environment where inflation is outpacing the coupons being paid. We believe that the solution is overweighting real assets that have historically been able to keep pace with inflation. In addition, for a portion of your portfolio, seeking out less-liquid assets that pay an illiquidity premium can do a lot to help boost returns. So while current trends are worrisome, if inflation does end up in a more permanent vs. transitory camp, we have diversified and attempted to build in potential protections into portfolios wherever possible.

Please reach out to your Morton wealth advisory team if you have any questions or would like to discuss any of these topics further. As always, we appreciate your continued confidence and trust.

Best Regards,

Morton Investment Team

Form ADV Brochure Update

We recently updated our ADV Part 2A filing to reflect some material changes since our last filing in March. The updated ADV Brochure can be accessed via this link.

If you have any questions, or wish to receive a paper copy of our ADV Part 2A Brochure, please email clientservices@mortoncapital.com or call us at (818) 222-4727 and we will be happy to assist you.

Disclosures:

Information presented is for educational purposes only and is not intended as an offer or solicitation with respect to the purchase of any security or asset class. This presentation should not be relied on for investment recommendations. Certain investment opportunities discussed herein may only be available to eligible clients. References to specific investments are for illustrative purposes only and should not be interpreted as recommendations to purchase/ sell such securities. This is not a representation that the investments described are suitable or appropriate for any person. It should not be assumed that MC will make investment recommendations in the future that are consistent with the views expressed herein. MC makes no representations as to the actual composition or performance of any security.

Although the information contained in this report is from sources deemed to be reliable, MC makes no representation as to the adequacy, accuracy or completeness of such information and it has accepted the information without further verification. No warranty is given as to the accuracy or completeness of such information.

The indices referenced in this document are provided to allow for comparison to well-known and widely recognized asset classes and asset class categories. YTD returns shown are from 12-31-2020 through 09-30-2021 and Q3 returns are from 07-01-2021 through 09-30-2021. Index returns shown do not reflect the deduction of any fees or expenses. The volatility of the benchmarks may be materially different from the performance of MC. In addition, MC’s recommendations may differ significantly from the securities that comprise the benchmarks. Indices are unmanaged, and an investment cannot be made directly in an index.

Past performance is not indicative of future results. All investments involve risk including the loss of principal.