December 2021

Looking back to other times in our history when the levels of federal debt were high, we find similarities to our current challenges. The federal government's fiscal strategies used previously are being redeployed to handle the high debt levels again today.

Specifically, it appears that we may be entering an interest rate/inflation scenario similar to post-WWII. At that time, two conditions were true:

· Inflation rates decoupled from interest rates (that could be earned from, say, Treasury notes).

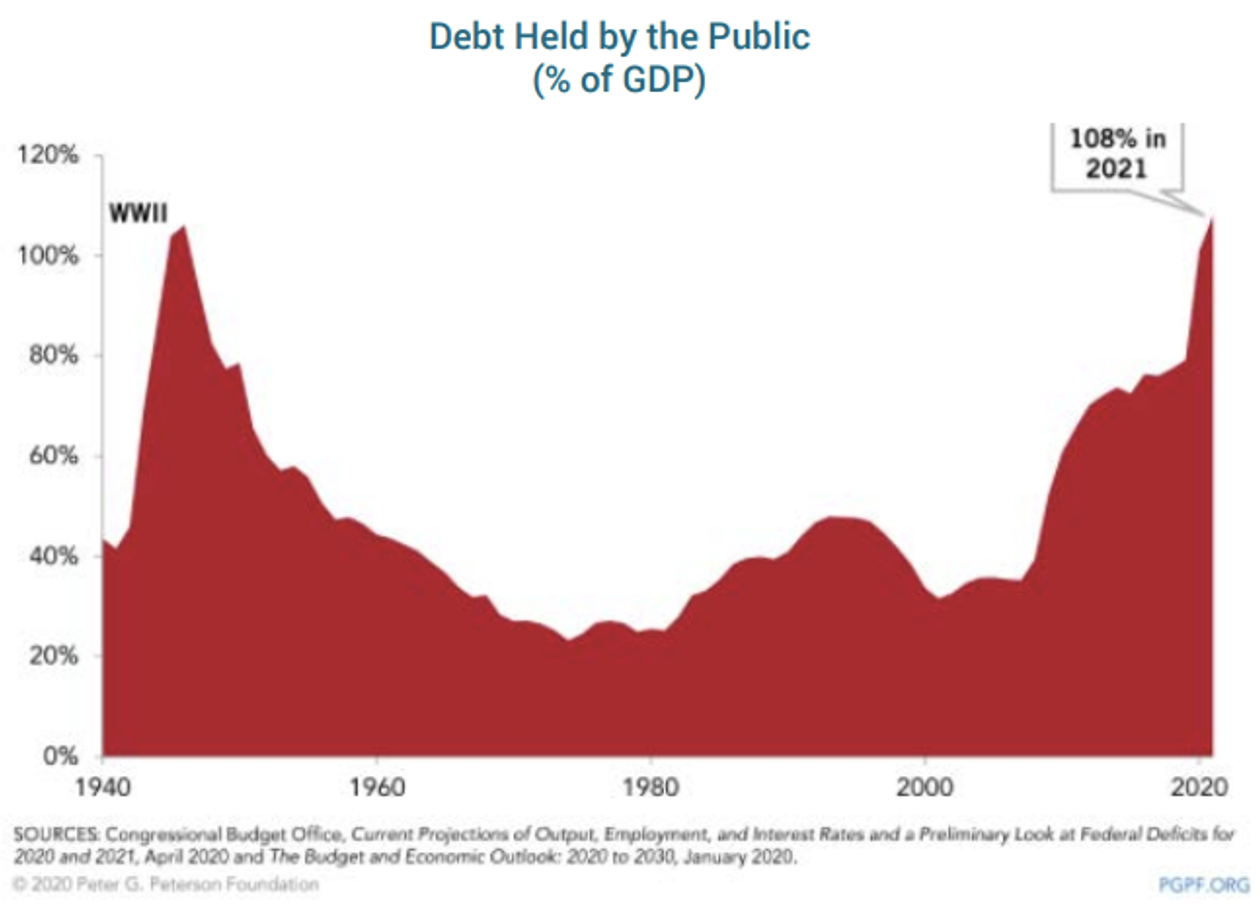

· Simultaneously, the federal debt was more than 100% of the country’s annual gross domestic product (GDP).

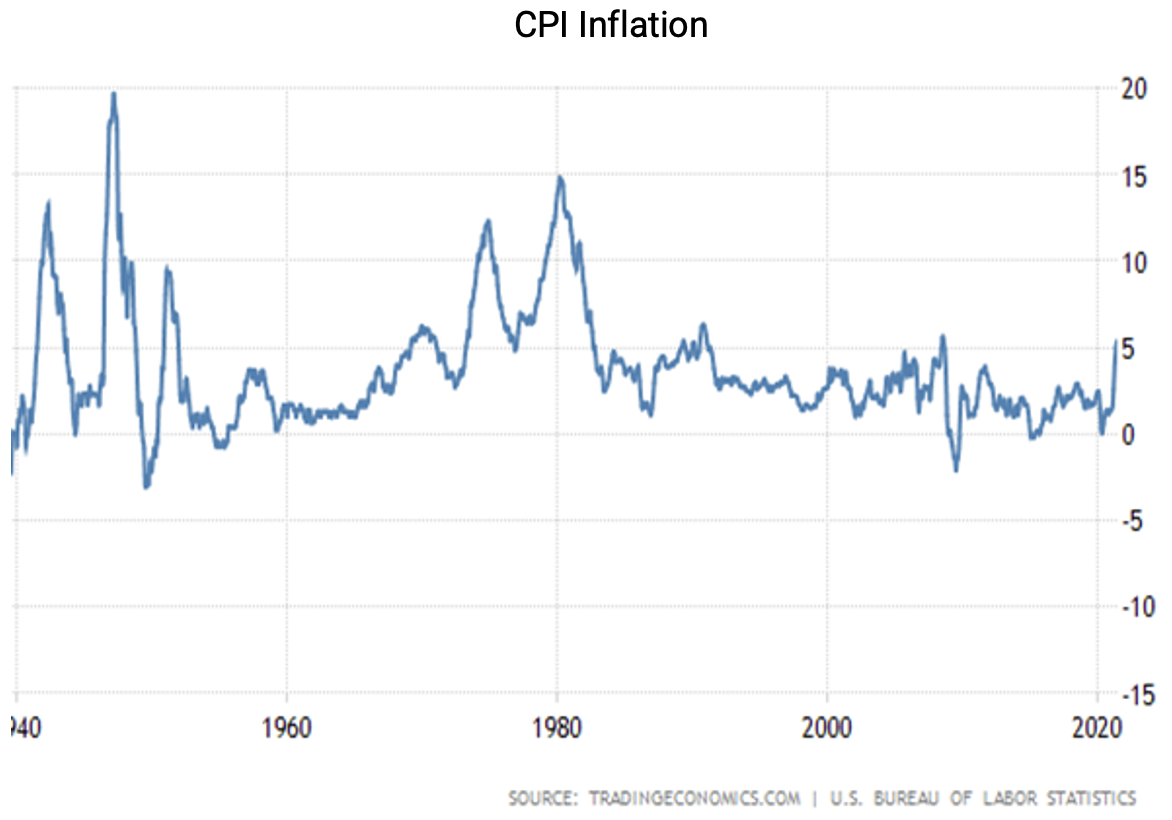

Historically, it has been “normal” to earn inflation-level returns in the bond market. For example, you may recall that in 1980, inflation was 15%, but you could still buy a Treasury note and earn that same 15%. Moving forward 20 years to 2000, you could still earn Treasury yields that met or exceeded inflation. This is no longer the case. Nor was it the case immediately following WWII.

In the late 1940s, inflation spiked into the high teens. Over the course of that entire decade, the Consumer Price Index (CPI), a common measure of inflation, moved up a total of 69%. Meanwhile, from 1940 to 1955, the yields on 10-year Treasury notes remained at a paltry 2.5%. With such low returns, fixed-income investors could not keep pace with inflation, meaning that traditional fixed-income assets eroded considerably in purchasing power.

Just recently, in the 12 months through November 2021, the CPI rose 6.8%. This is a level substantially higher than safe bond yields, as the 10-year Treasury barely even offered any income paying roughly 1.5%.

The current federal debt-to-GDP ratio, akin to post WWII, is again above 100%. To help pay down the debt in the 1940s, income tax rates started moving up. In 1941, the lowest tax bracket was 10%. By 1946, the lowest rate had risen to 20% and the highest rate was raised to 91%. As you are aware, bills currently under consideration in Congress are contemplating income tax increases.

The 1940s game plan was very successful at bringing down the level of federal debt to GDP. This was partially achieved by increased federal income tax revenues on inflated salaries and wages at the higher tax rates. Today, articles on higher wages appear daily in the press.

The circumstances of this “Great Decoupling” have implications for portfolio strategy—these dynamics make us interested in building portfolios around real assets, such as real estate (and a bit of gold), that can rise with inflation, including lending strategies (i.e., income-generating investments) on such real assets.

Read Bruce's other articles here:

An Advisor's Annotated Book Stack

Set It and Forget It - Not the Outcome You Thought You'd Get

Disclosures:

This information is presented for educational purposes only and is not intended as an offer or solicitation with respect to the purchase of any security or asset class. The views and opinions expressed by the author are as of the date of the recording and are subject to change. Morton Capital makes no representation that the strategies described are suitable or appropriate for any person.

These views are not intended as a recommendation to buy or sell any securities, and should not be relied on as financial, tax or legal advice. You should consult with your attorney, finance professional or accountant before implementing any transactions and/or strategies concerning your finances.

Some of the investment opportunities discussed are available to eligible clients and can only be made after the client’s careful review and completion of the applicable Offering Documents.Each investment opportunity is unique, and it is not known whether the same or similar type of opportunity will be available in the future. It should not be assumed that MC will make investment recommendations in the future that are consistent with the views expressed herein. MC makes no representations as to the actual composition or performance of any security.

Although the data referenced in this report is from sources deemed to be reliable, MC makes no representation as to the adequacy, accuracy or completeness of such information and it has accepted the information without further verification. No warranty is given as to the accuracy or completeness of such information.

Past results are no guarantee of future results. All investments involve risk including the loss of principal.